MACRO PULSE: FOOT-AND-MOUTH DISEASE

Economic Risks for Namibia

REGIONAL CONTEXT AND ESCALATING TRADE RISK

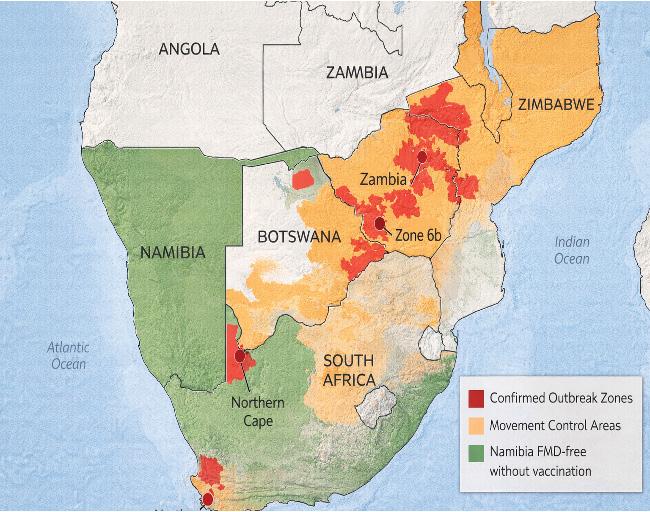

Recent FMD outbreaks in South Africa, Botswana and Zambia have elevated biosecurity from a sector-specific concern to a macroeconomic issue. A confirmed outbreak in South Africa’s Northern Cape, roughly 400 kilometres from Namibia’s southern border, together with infections in Botswana’s Disease Control Zone 6b, places Namibia within an intensified transboundary risk environment.

Botswana’s experience illustrates how rapidly FMD translates into trade restrictions. Following confirmed cases, fresh bovine meat exports to the UK were temporarily restricted and movement bans imposed within days, demonstrating how quickly animal-health events disrupt access to premium markets.

Namibia’s agricultural sector has historically shown significant volatility, with output ranging from strong expansions to contractions exceeding 20% during severe droughts. This structural fragility means an FMD-related export shock would compound an already cyclical recovery phase.

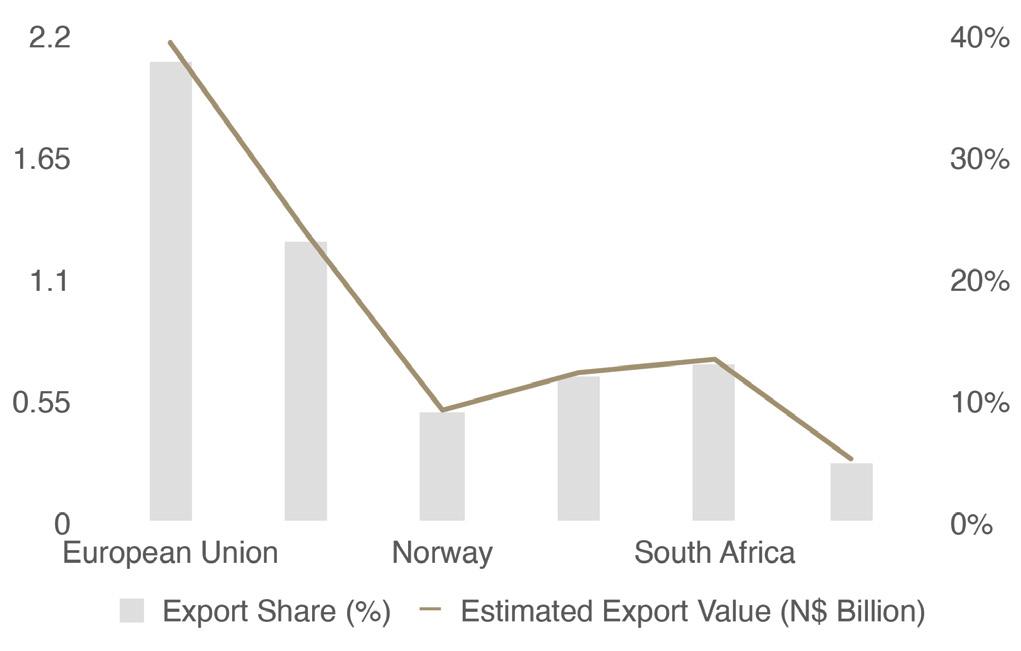

The livestock sector, valued at approximately N$15–17 billion, underpins export earnings, rural employment and regional income stability. Namibia’s export-approved abattoirs supply the EU, UK, Norway, South Africa and China. In 2024, Namibia exported an estimated 22.7 million kilograms of beef, with the EU and UK accounting for 55–65% of volumes. Beef exports are valued at roughly €290 million (N$5.7 billion annually), of which N$3–3.6 billion is directly exposed to EU and UK markets. A confirmed outbreak would likely trigger immediate export suspensions, with reinstatement typically requiring 12–24 months or longer.

Namibia’s exposure is amplified by timing. Severe drought in 2023 forced widespread destocking, and improved rainfall since late 2024 has initiated herd rebuilding, a phase involving greater livestock movements, auction activity and cross-border exposure precisely when regional disease risk is elevated.

CROSS-BORDER MOVEMENTS AND TRADE DISRUPTION LESSONS

Botswana’s outbreak demonstrates how quickly FMD translates into trade disruption. Following confirmed cases, strict movement bans were imposed and importing partners restricted fresh bovine meat, generating income losses and reputational damage.

For Namibia, disease-free credibility is economically valuable but fragile. Namibia maintains FMD-free status without vaccination, a premium classification supporting higher export prices and buyer confidence. Losing this status would halt exports and reduce prices upon re-entry.

Even without domestic infections, regional outbreaks affect Namibia through trade linkages. South Africa accounts for 35–40% of Namibia’s imports (over US$2.8 billion annually), and disruptions in South Africa’s livestock sector can lead to stricter inspections, higher compliance costs and supply inefficiencies.

FOOD PRICES, INFLATIONARY PRESSURES AND SECOND-ROUND EFFECTS

Food and non-alcoholic beverages account for 16.5% of Namibia’s CPI basket, with meat at 3.5% and beef at 1.3%. A 15% beef price increase could add 0.20 points to headline inflation; with poultry substitution adding 0.09 points, protein volatility could raise inflation by ~0.3 percentage points under stress.

In mid-2025, beef prices rose over 12% year-on-year despite no domestic outbreak. Given poultry’s CPI weight of 0.9%, substitution-driven increases amplify food inflation beyond the red-meat shock.

Second-round effects include adjusted inflation expectations, defensive retail pricing, wage pressure and tighter credit for farmers and processors.

MACROECONOMIC AND EMPLOYMENT IMPLICATIONS

Agriculture contributes approximately 6–8% of GDP but supports 20–23% of the labour force, compared with mining, which employs less than 5%. The livestock value chain supports 70,000–90,000 livelihoods, including farming households, abattoir workers, transport operators and veterinary services.

A 10% livestock output contraction due to export suspension could reduce GDP by 0.45 percentage points directly, with spillovers into processing potentially reaching 0.5–1.0 points. A prolonged suspension of N$5–6 billion in annual exports would widen the trade deficit, compress rural incomes and weaken manufacturing output.

GOVERNMENT PREPAREDNESS AND THE ECONOMICS OF PREVENTION

Namibia has adopted stricter border inspections, movement controls and expanded veterinary surveillance. Prevention spending should be viewed as risk insurance; the fiscal cost is modest relative to potential losses of billions in export revenue. Biosecurity functions as macroeconomic infrastructure rather than purely veterinary administration. A domestic outbreak would require additional fiscal resources for vaccination, compensation and surveillance, while reduced profitability would weaken tax contributions and increase stress in agricultural loan portfolios.

CONCLUSION: BIOSECURITY AS ECONOMIC INFRASTRUCTURE

Under a six-month export suspension, losses could reach N$2.5–3 billion with GDP growth reduced by 0.5 points and food inflation rising 0.2–0.3 points. A 12-month suspension could see losses approach N$5–6 billion, reducing GDP growth by up to 1 percentage point.

The regional FMD outbreak is a trade-linked biosecurity shock during a sensitive agricultural recovery phase. Safeguarding Namibia’s FMD-free status protects a sector worth N$15–17 billion, exports exceeding N$5–6 billion annually, and up to 90,000 livelihoods. Biosecurity preservation should be treated as core economic infrastructure requiring sustained vigilance and coordinated policy response.

Simonis Storm is known for financial products and services that match individual client needs with specific financial goals. For more information, visit: www.sss.com.na